If you thought 2024 was busy in senior housing and skilled nursing M&A, 2025 just rewrote the record books.

Publicly announced senior care transactions hit

871 deals in 2025, blowing past 2024’s record of 721. Even more impressive? The fourth quarter alone logged 285 transactions — the highest quarterly total ever recorded. October set a monthly record with 110 deals.

And here’s the kicker: the tailwinds heading into 2026 are stronger.

So what happened? And more importantly — what does it mean for operators, owners, and investors?

Let’s break it down.

Liquidity Returned — And Buyers Came Back Aggressive

The second half of 2025 felt like a switch flipped.

Lower capital costs. Rate cuts. Banks competing again. Debt funds getting aggressive. Fannie, Freddie and HUD stepping back into the arena. The 10-Year Treasury hovering near 4.1% provided some stability. The result? Confidence.

Sellers who held through the chaos of 2022–2024 finally felt comfortable bringing assets to market. Many had improved operations while waiting. Buyers, meanwhile, were eyeing the demographic surge and the near standstill in new development.

When you mix pent-up sellers with hungry buyers and available capital, you get bidding wars. Cap rates compressed — especially for stabilized Class-A assets — by 50 to 100 basis points in the second half of the year.

For context, newer assisted living and independent living communities averaged cap rates in the low 7% range in 2024. By late 2025, pricing pressure was clearly upward.

Occupancy Momentum Is Real

Another quiet driver of valuation strength: occupancy.

National occupancy reached 88.7% in Q3 2025, marking the 18th consecutive quarterly increase. That kind of sustained census growth changes underwriting assumptions fast.

With limited new construction in the pipeline, strong demand is colliding with constrained supply. That dynamic is pushing both NOI and asset values higher — particularly for high-quality product.

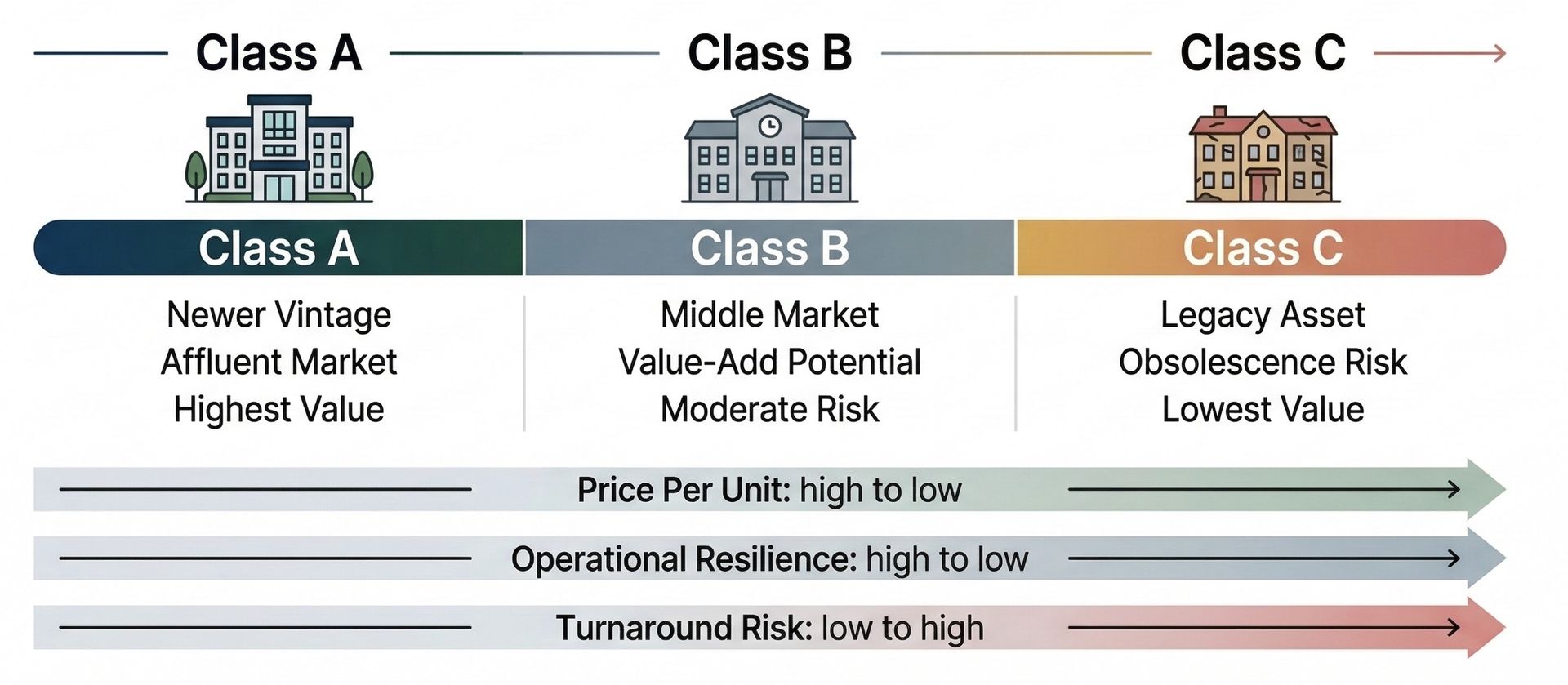

Class-A stabilized communities dominated investor interest in 2025. Baby boomers want newer buildings, strong amenities, and quality care environments. Capital is chasing exactly that.

Portfolio Deals Are Back

In 2023 and 2024, large portfolio sales were often broken apart due to financing challenges and distressed assets dragging valuations down.

That changed.

Investor confidence returned in late 2024, and by 2025 large portfolio transactions surged back. Companies are chasing scale again. And lenders are more willing to finance it.

One of the most notable moves: Sonida Senior Living’s acquisition of CNL Healthcare Properties’ 69-community portfolio. Post-closing, Sonida will become the eighth largest owner of senior housing assets in the country.

Scale matters. Operational efficiency matters. Balance sheet strength matters.

But scale alone doesn’t guarantee success — as Blackstone’s multi-year losses in seniors housing reminded everyone. This is still an operationally intensive business. Execution is everything.

Skilled Nursing: Stable, Strategic, Selective

While seniors housing saw explosive growth, skilled nursing M&A volume was relatively flat year over year — up just 3%.

But that’s not weakness. Skilled nursing never saw the same freeze that seniors housing did. It stayed active through the capital markets volatility.

Strong Medicaid rate increases in many states, limited bed supply, and improving reimbursement sentiment are supporting valuations. Large REIT buyers like Welltower and Omega Healthcare Investors were active in SNF acquisitions and joint ventures.

State-level dynamics still drive SNF valuations heavily — reimbursement rates, certificate-of-need laws, labor markets, regulatory environments. It’s hyper-local underwriting.

But long-term fundamentals? Solid.

REITs Flexed Their Muscle

Public healthcare REITs had a strong year — both in acquisitions and stock performance.

Welltower was in a league of its own, announcing nearly $14 billion of gross investments closed or under contract. Its stock rose almost 50% in 2025, following strong gains in 2023 and 2024.

Ventas also leaned heavily into Class-A stabilized assets, particularly SHOP structures, and posted solid NOI growth.

American Healthcare REIT, CareTrust, Omega, Sabra — most posted positive total returns and remained active buyers.

The public capital markets clearly rewarded growth, operational gains, and disciplined capital allocation.

Financing Markets Opened Up — But Development Still Tight

Agency lending — particularly HUD 232/223(f) — was active again in 2025. Bridge-to-HUD structures were common. Freddie Mac and Fannie Mae re-entered more competitively.

Conventional lenders increased activity on acquisitions and refinances.

Development, however, remains tough.

Construction costs are high. Deals need strong sponsorship and prime markets to pencil. Some projects are moving forward, but widespread speculative development isn’t happening yet.

Ironically, that lack of development is one reason existing stabilized assets are commanding stronger pricing.

What Does 2026 Look Like?

Could 2026 break records again?

It sounds ambitious. But 2025 surprised most observers.

Momentum isn’t just about transaction count. It’s about buyer depth, seller confidence, capital availability, occupancy trends, and pricing resilience. On those fronts, the sector looks strong.

Unless there’s a major macro shock, the demographic wave combined with minimal new supply suggests continued upward pressure on occupancy and asset values.

Expect:

- Continued cap rate compression for Class-A stabilized assets

- More buyers moving into Class-B and value-add plays

- Larger portfolio transactions

- Further REIT and institutional capital participation

- Strategic consolidation among operators

The senior housing and care industry is entering a new phase — one driven less by distress and more by strategic growth.

For investors and operators, the message is simple:

This market isn’t cooling down.

It’s accelerating.