The latest senior care market news reads a little like a packed auction room: more buyers, higher prices, fewer easy deals, and a lot of capital trying to find a home. That may sound intimidating, but for investors who know where to look, it is also a signal. The senior market is no longer a sleepy niche. It is becoming a serious institutional asset class — and the amateurs are going to get outbid, outmaneuvered, or both.

1. Seniors Housing M&A Is Hot — Maybe Too Hot

The big headline: seniors housing M&A activity and valuations are hitting record levels. Buyers are chasing occupancy recovery, stronger revenues, limited new construction, and the incoming demand wave from aging baby boomers.

Investor implication:

Do not expect bargain pricing on clean, stabilized assets. Those deals are getting crowded fast. The better play may be finding assets with fixable problems: weak marketing, tired interiors, poor operator alignment, or under-managed rates. In other words, buy the headache — but only if you know how to cure it.

2. Skilled Nursing Has Demand, But Not Enough Sellers

The SNF market is in a strange spot. Buyers want facilities, but many owners are holding because operations are better, reimbursement has improved, and off-market deals are becoming more common. Sabra’s CEO noted that their skilled nursing deals were “100% off market through existing relationships.”

Investor implication:

Relationships are becoming the new broker packet. If you are waiting for the perfect SNF deal to hit your inbox, good luck — you and 47 other buyers will be opening the same PDF. The edge is in operator relationships, direct seller conversations, and creative deal structures.

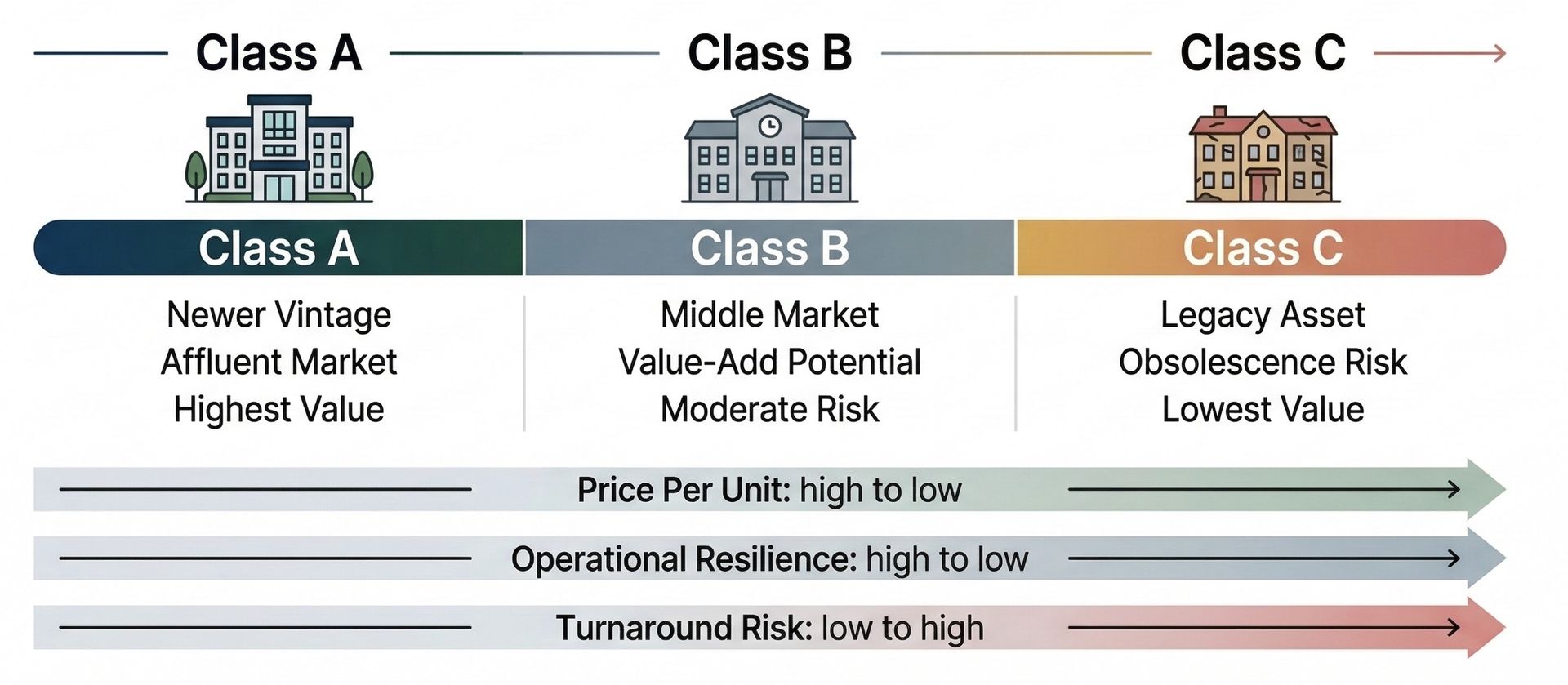

3. Class A Is Expensive, So Capital Is Moving Down the Quality Curve

Class-A senior housing is drawing the strongest competition, pushing some investors toward Class-B assets. But even Class-B is getting more attention now. The newsletter notes that as Class-A bidding intensifies, many investors are being forced down the quality curve, creating more competition there too.

Investor implication:

Class B may be the sweet spot, but only if the bones are good. Look for decent locations, manageable CapEx, and operating upside. Avoid “Class C pretending to be Class B” unless the discount is real. Lipstick on a 30-year-old building is still lipstick. Sometimes it is even cheap lipstick.

4. Standalone Memory Care Is Tricky — But Not Dead

The buyer pool for standalone memory care is thinner, but strong performers can still command real attention. Blueprint closed a record-setting sale of two standalone memory care communities in New York, supported by strong cash flow and an experienced incumbent operator.

Investor implication:

Memory care still works when the market, operator, staffing model, and reputation line up. But it is not a passive real estate deal. It is an operating business wearing a real estate jacket. Underwrite the operator as hard as the building.

Bottom Line

The senior market is moving from recovery mode into competitive growth mode. The easy money was buying distress when nobody wanted it. The next money will be made by investors who can source quietly, underwrite honestly, and partner with operators who can actually execute.

The punchline: this is still a great space — but the market is no longer handing out participation trophies.